Chapter 6Profit meets impact

Net impact data is not just for “doing good”

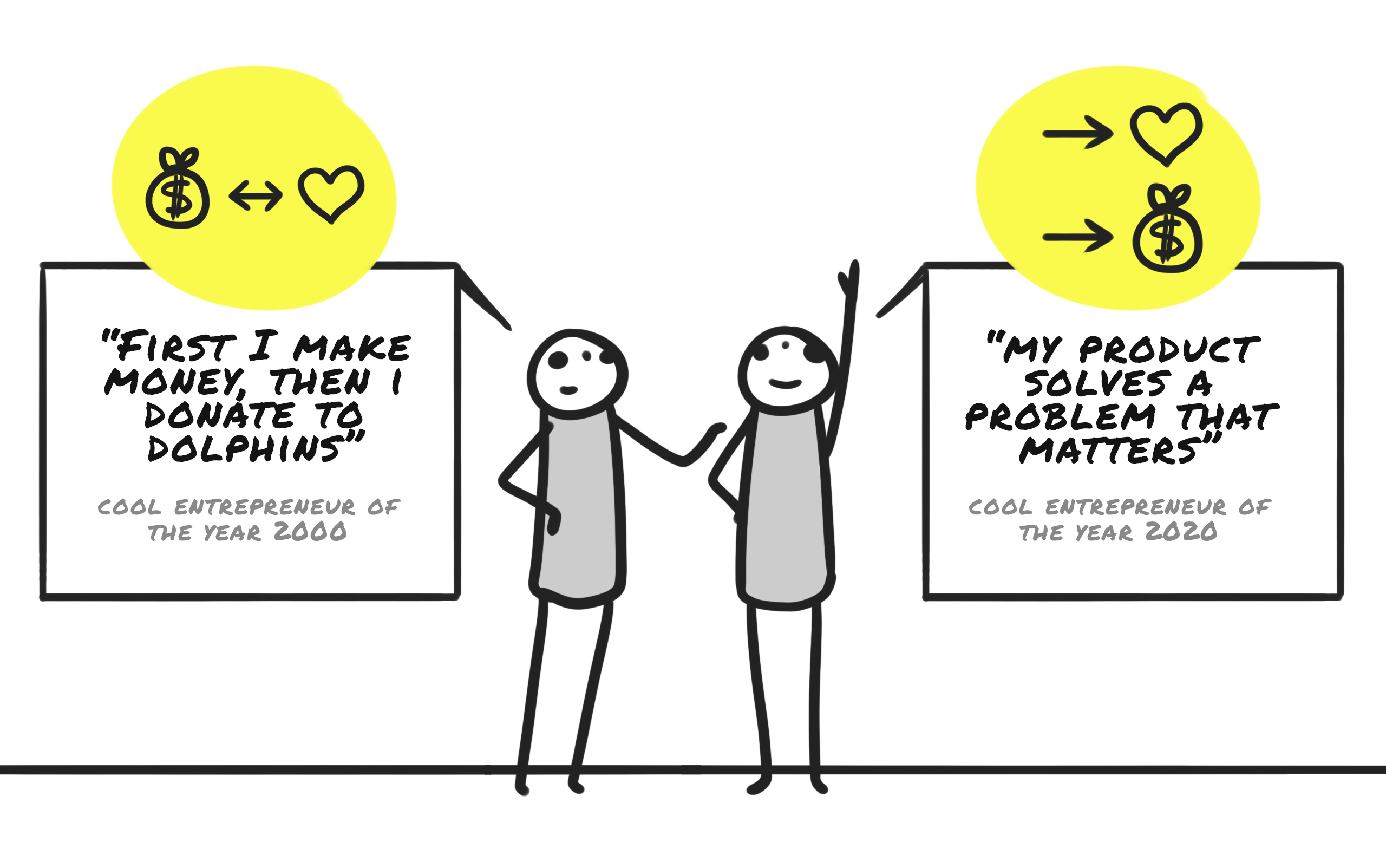

According to traditional thinking, companies ought to focus on profit. When this is done, some money will be left over for good causes, or "impact". An oil refinery that is doing well, for example, might install solar panels on the roof of its headquarters to keep the office lights on with solar power. Or a candy manufacturer might switch its production lines to work with renewable energy.

In this way of thinking, impact is essentially an additional OPEX expense, and fundamentally at odds with maximizing profits: impact and EBITDA point towards opposite directions.

Luckily this genre of business logic has already seen its best days. In the new way of thinking, companies align their impact to point in the same direction with their EBITDA. That means that they offer products and services with intrinsically net positive value creation meachanisms, creating positive impact while at the same time making good money for the company's owners. When such a business grows, its positive impact automatically increases, without any separate artificial "impact projects".

Is impact still at odds with profits?

Upright's mission is to incentivize companies to optimize their net impact. Simply stated, this means trying to make it easier for net positive companies to make healthy profits, and harder for net negative companies to do the same.

Consumers, investors, and employees are now putting increasing pressure on companies to begin considering the impact of what they do. This fact was clear from the results of Upright's Impact at Work employee survey: on average, respondents stated that companies with a negative impact should expect to pay a 85% premium on salaries, whereas companies with a positive impact can expect to save 15%.

Given this atmosphere, is it easier today to make a profit by running a business with a net positive net holistic impact? Figure 6.2, which shows the net profit ratios of Fortune Global 500 companies plotted against their net impact ratios, can offer us a hint on the answer.

In this data we find a small, but statistically significant (p-value = 2.5e-8, spearman correlation = 0.23) positive correlation between impact and profit. Curiously, the correlation is higher (spearman correlation = 0.38) when net impact ratio is replaced with the net score for the environment category (Figure 6.2). This suggests that creating negative environmental impacts in particular can make it increasingly difficult to sustain profits.

However, given that net profit ratios are affected by a complex set of partially random intertwining factors, such as competition landscape, industry cost structure, operative efficiency and corporate legacy, one should not use this data to conclude that improving impact somehow automatically leads to improvements in profits. (We are working on some pretty exciting analyses in this area - if you’re interested in them, subscribe to our newsletter to get updates using the button below.)

What is safe to conclude, however, is that making a positive impact is definitely not at odds with making profits. There is therefore no excuse for anyone to ignore impact for "business reasons" any longer, be it an asset manager setting asset allocations of equity funds, a CEO deciding on product strategy, or an aspiring young entrepreneur dreaming up a new business idea.